By Mike Allen, CFP® · Managing Partner, Security Financial Management · CRD #3153161

Reviewed by Dave Allen, CFP® · CRD #1210763 · July 6, 2026 · Last reviewed July 6, 2026

Securities offered through Kestra Investment Services, LLC, member FINRA/SIPC (Kestra IS). Investment advisory services offered through Kestra Advisory Services, LLC (Kestra AS). Security Financial Management, Bluespring Wealth Partners, LLC, Kestra IS and Kestra AS are affiliated through common ownership by Kestra Holdings.

Why Most Roth Conversions Fail Coordination Math (Not Market Timing)

The Market-Timing Trap

Most households think about Roth conversions as a market-timing question. Equities are down — convert now, the thinking goes, because the tax bill is lower on the depressed valuation and the future recovery happens inside the Roth. The logic is sound in a single year. It collapses across a multi-year horizon, because the variable that drives whether a conversion was worth doing is not the equity print on the conversion day. It is the household’s effective tax rate across the entire window between the conversion year and the year RMDs begin — and beyond.

This is the same pattern we named last month as the Coordination Pattern: a decision that looks correct in isolation, but stops agreeing with the rest of the plan as soon as a second variable enters the math. Estate documents drift out of coordination year by year. Tax decisions drift out of coordination bracket by bracket. The mechanism is the same. The variable is different.

Introducing the Bracket-Window Audit

The Bracket-Window Audit is the framework we use to size conversions for $1M–$3M households. It is the practice of modeling household income across the multi-year tax-bracket window — not against this year’s print, but against the entire stretch between the household’s current age and three years past their RMD onset. That window is usually eight to fifteen years. The output is not “convert this much.” It is “convert this much in each of these years, with these IRMAA, RMD, and capital-gains interactions noted.”

The audit answers four questions in sequence:

- How much room is left in this year’s target bracket? The 2026 federal income tax schedule — released by the IRS in October 2025 — caps the 24% bracket at $403,550 for married couples filing jointly. The space between this year’s run-rate income and that ceiling is the conversion capacity in the 24% bracket. The 32% ceiling sits at $250,525 of taxable income for single filers and the analogous MFJ threshold above — that is the next bracket window when the 24% room is exhausted.

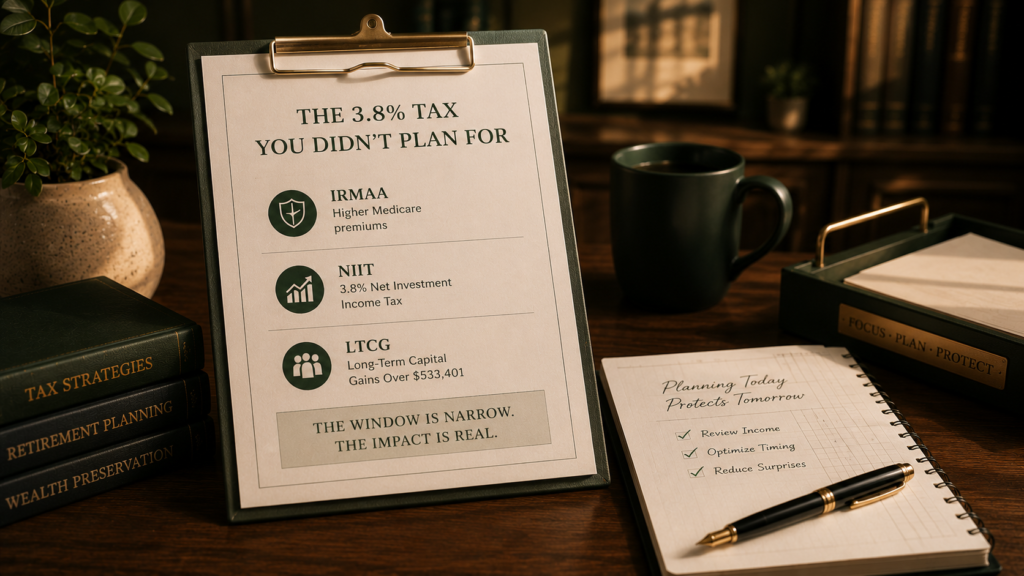

- Will this year’s conversion move 2028 Medicare premiums? The Centers for Medicare and Medicaid Services apply a two-year MAGI lookback to IRMAA. The 2026 first IRMAA threshold sits at $109,000 MAGI for single filers and $218,000 for married filing jointly, with the top tier capping at $500,000 / $750,000. A conversion that pushes MAGI $1 over a threshold moves the entire year into the next IRMAA tier — IRMAA is a cliff, not a slope.

- How many years until RMDs begin? Under SECURE Act 2.0, the RMD onset age is 73 for households born between 1951 and 1959, and rises to 75 for those born in 1960 or later (effective 2033). Every year remaining in the pre-RMD window is a conversion year that does not compete with RMD income for bracket space.

- Is there 0% capital gains bracket room this year? The 2026 zero-rate long-term capital-gains ceiling sits at $98,900 of taxable income for married filers and $49,450 for single filers. A household with appreciated taxable assets and unused 0% LTCG room may be better off realizing the gain than executing a conversion — or doing both in sized proportion. The two decisions compete for the same bracket space.

Why the Multi-Year View Matters

A household that converts $200,000 in a single year may pay a marginal 24% on most of it — and trigger a $4,800 IRMAA surcharge for the following two years because they crossed a tier. The same household, modeled across four years at $50,000 per year, may stay below the IRMAA threshold every year and pay the same 24% marginal rate without the surcharge. Same conversion amount. Same marginal bracket. Different total tax bill — because the second model coordinates across years and the first does not.

This is what the One Big Beautiful Bill Act made permanent in 2026 reframes. With TCJA’s sunset removed and the bracket schedule made permanent, the urgency of “convert before brackets reset” is gone. What remains — and what becomes the central planning question — is the multi-year coordination math.

What This Means for Planning This Month

July is the month the model gets built — not the month conversions get executed. Q2 income is now visible. Q3–Q4 bracket capacity can be modeled with high confidence. The IRMAA decision for 2028 premiums is being made now whether the household knows it or not, because 2026 MAGI is the input that determines it. The window to coordinate the decision while there is still room to size it is open through September.

The practical walkthrough — the five decisions and the order to run them in — sits in this month’s companion piece: Read the Mid-Year Tax Decision Audit.

Frequently Asked Questions

The math is largely independent of equity drawdown. The variables that drive whether a conversion is worth doing are the household’s marginal bracket this year, IRMAA tier exposure, years until RMD onset, and the capital-gains and basis picture — not the level of the S&P 500 on the conversion day.

Because the household’s personal rate is still rising — through Social Security taxation, RMDs at age 73 or 75, and survivor filing-status compression. The OBBBA bracket schedule is permanent. The household’s place inside that schedule is not. Conversion moves the rate at which an asset gets taxed from a higher future rate to a known current rate.

No. The Tax Cuts and Jobs Act eliminated Roth recharacterization in 2018, and OBBBA did not restore it. A Roth conversion is final on the day it is processed. This is the structural reason multi-year modeling matters — there is no correction path if the year’s conversion turns out to be the wrong size.

The Bracket-Window Audit answers this directly. The right size in any given year is the amount that fills the targeted bracket without crossing into the next IRMAA tier, without crowding 0% LTCG room you intended to use, and without competing with an RMD that has already started. For households inside three years of RMD onset, the right size is usually larger than it feels. For households eight or more years from RMD onset, the right size is usually smaller than it feels.

Continue with the July Coordination Pillar

- Read the Resource: The Mid-Year Tax Decision Audit — Five Decisions Before September

- Listen to the Conversation: Roth Conversion & RMD Coordination — Best Advice Podcast Guys (publishes mid-July)

- Read the Market Commentary: Mid-Year Inflation, Rate Path, and Conversion Sizing (publishes Wed Jul 15)

- Read this month’s Brief: July 2026 — Tax Decision Coordination: The Month in One Read (publishes Tue Jul 28)

Next month — August 2026 — we move to the asset-side decisions: portfolio drift, rebalancing windows, and the cost-basis math that determines how taxes hit when assets actually move.

Schedule with Security Financial Management

A 15-minute call is the simplest way to see whether the household’s plan needs a Bracket-Window Audit before September, or whether the current trajectory is already coordinated.

About the Author

Mike Allen, CFP® · Managing Partner, Security Financial Management. Mike has guided Central Florida households through coordinated estate and retirement planning since joining SFM in 2007. Named to AdvisorHub’s 2024 Advisors to Watch (#47, Over $1B). 19 years of industry experience, zero disclosures.

Disclosures

The information presented is for educational purposes only and does not constitute legal, tax, or investment advice. Security Financial Management, Inc. is a registered investment advisor under Kestra Advisory Services, LLC. Tax planning strategies should be coordinated with qualified tax professionals familiar with your specific situation. Past performance is not indicative of future results.

Securities offered through Kestra Investment Services, LLC, member FINRA/SIPC (Kestra IS). Investment advisory services offered through Kestra Advisory Services, LLC (Kestra AS). Security Financial Management, Bluespring Wealth Partners, LLC, Kestra IS and Kestra AS are affiliated through common ownership by Kestra Holdings.